Spring cleaning feels great … once it’s finished. But getting there isn’t always so fun. To help you get to the enjoyable side of spring cleaning, we’ve rounded up some tips and tricks to streamline the process and leave you with more time to enjoy your fresh and tidy home.

1. ADD A LAZY SUSAN TO YOUR FRIDGE

If you’re already taking everything out to give the fridge a good scrub, add a lazy Susan to each shelf before you restock. Being able to spin it to access things in the back will cut down on spills and make your next spring cleaning that much easier.

2. DISINFECT YOUR SPONGE

If you’ve got a big job to do and only one sponge to do it with (the horror!), freshen things up halfway through by squeezing it out and microwaving it on high for a minute.

3. DON’T FORGET TO CLEAN THE GARBAGE DISPOSAL

If you’re lucky enough to have a garbage disposal, don’t neglect it during spring cleaning. Drop in a cut-up lemon, some salt, and a few ice cubes to clear away any unwanted odors or built-up residue.

4. TIME YOURSELF

ISTOCK.COM/OZ_MEDIA

Not only will you be more likely to stay focused and get your tasks done efficiently with a timer ticking, seeing how long chores actually take makes them more manageable. If you know it only takes 10 minutes to scrub the bathroom, maybe you won’t wait till next spring to do it again.

5. WAX YOUR STOVETOP

After you’ve scrubbed the grime off your stovetop, apply a thin layer of car wax and then buff it off with a clean towel. Not only will this make it look shiny and new, it will make wiping off future spills a breeze.

6. USE A LEMON TO CLEAN STAINLESS STEEL FAUCETS

Just cut the lemon in half and start rubbing to remove hard water stains and rust from any stainless steel in the bathroom or kitchen. Plus, this leaves behind a fresh, natural, citrusy scent instead of harsh chemical fumes.

7. STEAM-CLEAN YOUR MICROWAVE

To remove old food stains from the inside of the microwave, steam them before you scrub. Fill a microwave-safe bowl with 1 to 2 cups of water, 2 tablespoons of white vinegar, and a few drops of your favorite essential oil and zap the mixture for five minutes.

8. WASH YOUR WINDOWS ON A CLOUDY DAY

ISTOCK.COM/KOLDUNOVA_ANNA

For a quick made-at-home window-washing solution, mix equal parts white vinegar and warm water or add one teaspoon of mild dishwashing liquid to several gallons of water. But time your cleaning wisely: Sunshine will cause your windows to dry too quickly, leaving streaks.

9. MAKE SPACE FOR CLUTTER

One way you can ensure that your hard-earned neatness doesn’t disappear is by setting aside space for the inevitable clutter. If you have an entryway closet, mount a plastic or cloth shoe rack to store toys, hats, gloves, and unsorted mail.

10. DUST WITH FABRIC SOFTENER SHEETS

Dryer sheets are a cheap substitute for more expensive electrostatic cloths, and they work just as well. Lone socks that have lost their mates, when worn as a mitten, also work for dusting tight areas and Venetian blinds. Always remember to work top to bottom when dusting to avoid wasting time going over surfaces twice.

11. USE A HAIR DRYER TO BANISH WATER RINGS

Someone hasn’t been using a coaster and now your wood coffee table paid the price and has those telltale white water rings. Try erasing them with a hair dryer. Simply blast the offending spot on high heat until it starts to disappear. Once it’s gone, rub a little bit of olive oil on the area to recondition the wood.

12. TOSS EXPIRED TOILETRIES AND MAKEUP

ISTOCK.COM/INATIN1

If your medicine cabinet is starting to seem over-cluttered, spring cleaning is the perfect time to re-check the expiration date on all your toiletries and trash anything that’s past its prime. You can check the internet for specifics, but sunscreen should only stick around for a few years after you purchase it, and mascara should be replaced every couple of months.

13. USE YOUR DISHWASHER FOR MORE THAN DISHES

There are tons of things that you can clean in the dishwasher that don’t have anything to do with place settings. Once every few months, toss some of the following into the dishwasher for a deep clean: contact lens cases, hair brushes, makeup brushes, pet dishes, plastic kids toys, refrigerator shelves, soap dishes, tweezers, various knobs and pulls, and even your showerhead (if it’s removable).

14. CLEAN YOUR DISHWASHER

What good is a dirty dishwasher? After you remove any visible grime, place a (dishwasher safe) cup of vinegar on the top shelf and run the hottest cycle your dishwasher has. After that, sprinkle a cupful of baking soda around the bottom and run it through a short but complete cycle using the hottest water.

15. CLEAN YOUR SHOWERHEAD

ISTOCK.COM/GRANDRIVER

If your shower head isn’t detachable and thus can’t be run through the dishwasher, you can clean it by letting it soak in vinegar overnight. First, fill a sandwich baggie with vinegar and then carefully secure the bag over the shower head so it’s fully submerged—you can use an elastic hair tie or rubber band. Leave the whole thing to soak overnight—just be sure you remember to remove the vinegar bag before you turn on the shower in the morning!

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-09-28 16:00:502020-09-29 06:09:4815 Brilliant Spring Cleaning Hacks

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-09-28 16:00:462020-09-29 23:31:22Dave’s corner (These could be the best ones of the year)

Scamwatch has received over 4160 scam reports mentioning the coronavirus with over $3 360 000 in reported losses since the outbreak of COVID-19 (coronavirus). Common scams include phishing for personal information, online shopping, and superannuation scams.

If you have been scammed or have seen a scam, you can make a report on the Scamwatch website, and find more information about where to get help.

Scamwatch urges everyone to be cautious and remain alert to coronavirus-related scams. Scammers are hoping that you have let your guard down. Do not provide your personal, banking or superannuation details to strangers who have approached you.

Scammers may pretend to have a connection with you. So it’s important to stop and check, even when you are approached by what you think is a trusted organisation.

Visit the Scamwatch news webpage for general warnings and media releases on COVID-19 scams.

Below are some examples of what to look out for.

These are a few examples, but there are many more. If your experience does not match any of the examples provided, it could still be a scam. If you have any doubts at all, don’t proceed.

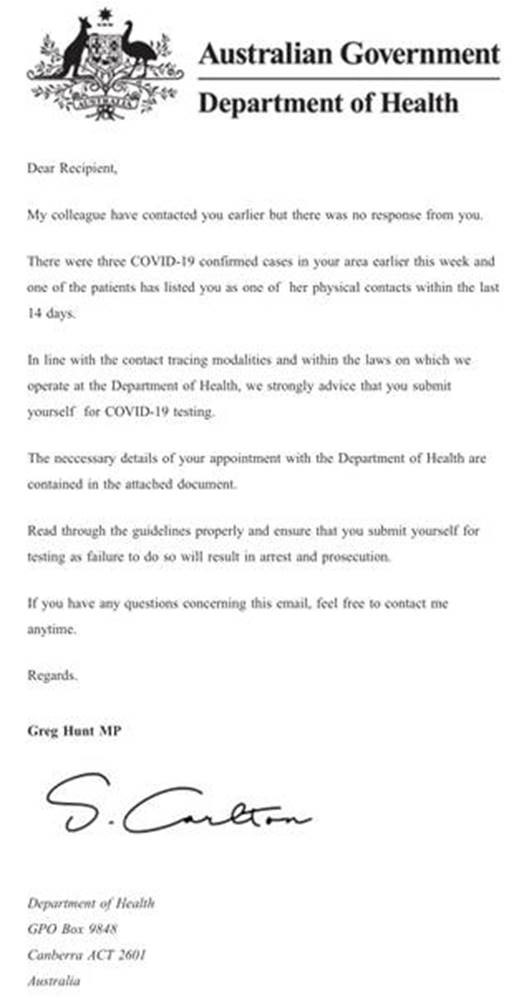

Phishing – Government impersonation scams

Scammers are pretending to be government agencies providing information on COVID-19 through text messages and emails ‘phishing’ for your information. These contain malicious links and attachments designed to steal your personal and financial information.

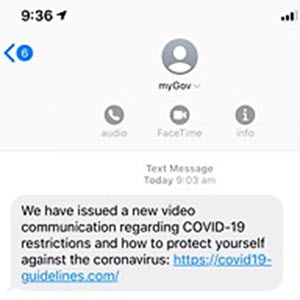

In the examples below the text messages appear to come from ‘GOV’ and ‘myGov’, with a malicious link to more information on COVID-19.

Examples of phishing scams impersonating government agencies

Department of Health impersonation email

Fake myGov texts

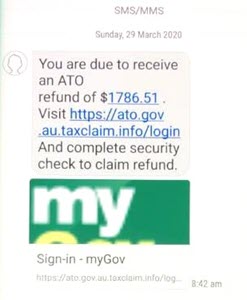

Scammers are also pretending to be Government agencies and other entities offering to help you with applications for financial assistance or payments for staying home.

Examples of payment or financial assistance scams

Fake government subsidy phishing scam

Fake ATO tax credit scam

Fake economic support payment text

Tips to protect yourself from these types of scams:

Don’t click on hyperlinks in text/social media messages or emails, even if it appears to come from a trusted source.

Go directly to the website through your browser. For example, to reach the MyGov website type ‘my.gov.au’ into your browser yourself.

Never respond to unsolicited messages and calls that ask for personal or financial details, even if they claim to be a from a reputable organisation or government authority — just press delete or hang up.

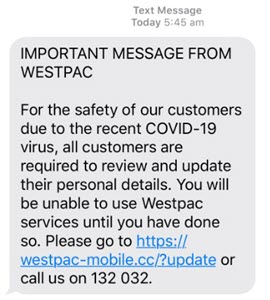

Phishing – Other impersonation scams

Scammers are pretending to be from real and well known businesses such as banks, travel agents, insurance providers and telco companies, and using various excuses around COVID-19 to:

ask for your personal and financial information

lure you into opening malicious links or attachments

gain remote access to your computer

seek payment for a fake service or something you did not purchase.

Examples of other phishing scams

Fake bank phishing text

Fake insurance phishing text

Fake voucher phishing text

Tips to protect yourself from these types of scams:

Don’t click on hyperlinks in text/social media messages or emails, even if they appear to come from a trusted source.

Never respond to unsolicited messages and calls that ask for personal or financial details — just press delete or hang up.

Never provide a stranger remote access to your computer, even if they claim to be from a telco company such as Telstra or the NBN Co.

To verify the legitimacy of a contact, find them through an independent source such as a phone book, past bill or online search.

Superannuation scams

Scammers are taking advantage of people in financial hardship due to COVID-19 by attempting to steal their superannuation or by offering unnecessary services and charging a fee.

The majority of these scams start with an unexpected call claiming to be from a superannuation or financial service.

The scammers use a variety of excuses to request information about your superannuation accounts, including:

offering to help you access the money in your superannuation

ensuring you’re not locked out of your account under new rules.

checking whether your superannuation account is eligible for various benefits or deals.

Example of a superannuation scam

A scammer will call pretending to be from a superannuation or financial service. They may refer to the government’s superannuation early release measures, and ask questions such as:

Have you worked full time for the last 5 years?

Are you going to apply for the $10 000 superannuation package?

Or falsely claim:

Inactive super accounts will be locked if not merged immediately.

Superannuation early-access scams

Many Australians are facing financial hardship due to the COVID-19 pandemic. On 22 March, the Australian Government announced eligible individuals would be allowed early access to their superannuation. Scammers are taking advantage of the government’s early-release measures in a variety of phishing scams designed to steal your superannuation.

Tips to protect yourself from these types of scams:

Never give any information about your superannuation to someone who has contacted you — this includes offers to help you access your superannuation early under the government’s new arrangements.

Hang up and verify their identity by calling the relevant organisation directly — find them through an independent source such as a phone book, past bill or online search.

For more information on superannuation scams visit ASIC’s MoneySmart website.

Online shopping scams

Scammers have created fake online stores claiming to sell products that don’t exist — such as cures or vaccinations for COVID-19, and products such as face masks.

Tips to protect yourself from these types of scams:

The best way to detect a fake trader or social media shopping scam is to search for reviews before purchasing. No vaccine or cure presently exists for the coronavirus.

Be wary of sellers requesting unusual payment methods such as upfront payment via money order, wire transfer, international funds transfer, preloaded card or electronic currency, like Bitcoin.

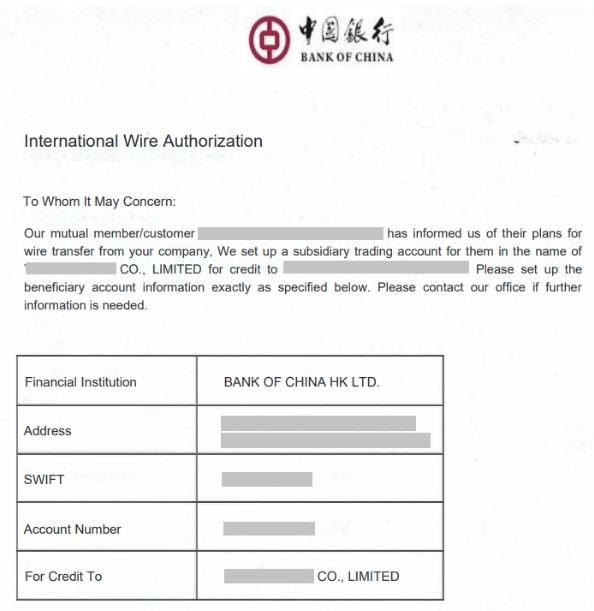

Scammers are using COVID-19 in business email compromise scams by pretending to be a supplier or business you usually deal with.

Scammers are using COVID-19 as an excuse to divert your usual account payments to a different bank account. Your payment goes to the scammer instead of the real business.

Example of a business email compromise scam

Tips to protect yourself from these types of scams:

Verify any request to change bank details by contacting the supplier directly using trusted contact details you have previously used.

Consider a multi-person approval process for transactions over a certain dollar amount, with processes in place to ensure the business billing you is the one you normally deal with.

Keep the security on your network and devices up-to-date, and have a good firewall to protect your data.

Businesses can also sign up to the ACCC’s Small Business Information Network to receive emails about new or updated resources, enforcement action, changes to Australia’s competition and consumer laws, events, surveys and scams relevant to the small business sector.

How scammers contact you

During a crisis like COVID-19, you may be isolated and using online services more than ever, so it is important to think about who might be really contacting you. They may find you by:

calling you or coming to your door

contacting you via social media, email or text message

setting up websites that look real, and impersonating government, business or even your friends

collecting information about you so that when they make contact they are more convincing.

How you can help others

You can help others by talking and sharing information about scams when connecting with your friends, family and colleagues.

Ask the businesses you connect with regularly about scams they see, how they can protect you and how you can protect yourself.

If you use social media or particular applications — learn how to report scams to them and choose services that will identify and remove scammers from their platform or website.

Ask your bank or financial institution about how to protect your financial information and how they will help you if you get scammed.

Government, law enforcement, individuals and businesses all play an important role in helping to protect the community from scams.

With the onset of Covid-19 and the resultant changes to accessing superannuation, there inevitably comes the opportunistic people who see the chance to take advantage of those in a vulnerable position.

Scamwatch has seen a 55 per cent increase in reports involving loss of personal information this year compared with the same period in 2019, totaling more than 24 000 reports and over $22 million in losses.

About

COVID-19 scams

Scamwatch has received over 3900 scam reports mentioning the coronavirus

with over $3.1 million in reported losses since the outbreak of COVID-19

(coronavirus). Common scams include phishing for personal information, online

shopping, and superannuation scams.

If you have been scammed or have seen a scam, you can make

a report on the Scamwatch website, and find more information

about where to get help.

Scamwatch urges everyone to be cautious and remain alert to

coronavirus-related scams. Scammers are hoping that you have let your guard

down. Do not provide your personal, banking or superannuation details to

strangers who have approached you.

Scammers may pretend to have a connection with you. So it’s important to

stop and check, even when you are approached by what you think is a trusted

organisation.

Visit the Scamwatch news webpage for general warnings

and media releases on COVID-19 scams.

Below are some examples of what to look out for.

These are a few examples, but there are many more. If your

experience does not match any of the examples provided, it could still be a

scam. If you have any doubts at all, don’t proceed.

Phishing

– Government impersonation scams

Scammers are pretending to be government agencies providing information

on COVID-19 through text messages and emails ‘phishing’ for your information.

These contain malicious links and attachments designed to steal your personal

and financial information.

In the examples below the text messages appear to come from ‘GOV’ and

‘myGov’, with a malicious link to more information on COVID-19.

Examples

of phishing scams impersonating government agencies

Department of Health impersonation email

Fake myGov texts

Scammers are also pretending to be Government agencies and other

entities offering to help you with applications for financial assistance or

payments for staying home.

Examples

of payment or financial assistance scams

Fake government subsidy phishing scam

Fake ATO tax credit scam

Fake economic support payment text

Tips

to protect yourself from these types of scams:

Don’t click on hyperlinks in

text/social media messages or emails, even if it appears to come from a

trusted source.

Go

directly to the website through your browser. For example, to reach the

MyGov website type ‘my.gov.au’ into your browser yourself.

Never

respond to unsolicited messages and calls that ask for personal or

financial details, even if they claim to be a from a reputable

organisation or government authority — just press delete or hang up.

Phishing

– Other impersonation scams

Scammers are pretending to be from real and well known businesses such

as banks, travel agents, insurance providers and telco companies, and using

various excuses around COVID-19 to:

ask

for your personal and financial information

lure

you into opening malicious links or attachments

gain

remote access to your computer

seek

payment for a fake service or something you did not purchase.

Examples

of other phishing scams

Fake bank phishing text

Fake insurance phishing text

Fake voucher phishing text

Tips

to protect yourself from these types of scams:

Don’t

click on hyperlinks in text/social media messages or emails, even if they

appear to come from a trusted source.

Never

respond to unsolicited messages and calls that ask for personal or

financial details — just press delete or hang up.

Never

provide a stranger remote access to your computer, even if they claim to

be from a telco company such as Telstra or the NBN Co.

To

verify the legitimacy of a contact, find them through an independent

source such as a phone book, past bill or online search.

Superannuation

scams

Scammers are taking advantage of people in financial hardship due to

COVID-19 by attempting to steal their superannuation or by offering unnecessary

services and charging a fee.

The majority of these scams start with an unexpected call claiming to be

from a superannuation or financial service.

The scammers use a variety of excuses to request information about your

superannuation accounts, including:

offering

to help you access the money in your superannuation

ensuring

you’re not locked out of your account under new rules.

checking

whether your superannuation account is eligible for various benefits or

deals.

Example of a

superannuation scam

A scammer will call pretending to be

from a superannuation or financial service. They may refer to the government’s

superannuation early release measures, and ask questions such as:

Have you worked full time for the last 5

years?

Are you going to apply for the $10 000

superannuation package?

Or falsely claim:

Inactive super accounts will be locked if not

merged immediately.

Superannuation

early-access scams

Many Australians are facing financial hardship due to the COVID-19

pandemic. On 22 March, the Australian Government announced eligible individuals

would be allowed early access to their superannuation. Scammers are taking

advantage of the government’s early-release measures in a variety of phishing

scams designed to steal your superannuation.

Tips

to protect yourself from these types of scams:

Never

give any information about your superannuation to someone who has

contacted you — this includes offers to help you access your

superannuation early under the government’s new arrangements.

Hang

up and verify their identity by calling the relevant organisation directly

— find them through an independent source such as a phone book, past bill

or online search.

For

more information on superannuation scams visit ASIC’s MoneySmart

website.

Online

shopping scams

Scammers have created fake online stores claiming to sell products that

don’t exist — such as cures or vaccinations for COVID-19, and products such as

face masks.

Tips

to protect yourself from these types of scams:

The

best way to detect a fake trader or social media shopping scam is to

search for reviews before purchasing. No vaccine or cure presently exists

for the coronavirus.

Be

wary of sellers requesting unusual payment methods such as upfront payment

via money order, wire transfer, international funds transfer, preloaded

card or electronic currency, like Bitcoin.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-09-28 16:00:372020-09-29 06:43:12Are you being scammed?

With the effect of the current environment and a number of other factors, we have recently been notified that some insurance premiums will increase by up to 100%. So if it has been a while since you have had your insurance reviewed, this should be the incentive to ensure your insurance cover is still suitable for your your situation. At Tailored Lifetime Solutions, we pride ourselves on being experts in insurance. We work to find the most cost-effective cover that meets your insurance needs.

Insurance might not always be top of mind, but it’s important to review your policies regularly to make sure you’ve got the right cover

Whatever your mix of cover — life, total and permanent disability, income protection and trauma — insurance can be an important part of protecting yourself and your family, now and into the future.

Thanks to the ability to pay for insurance through super, an estimated 94 per cent of working Australians have some level of life cover1. So it’s a good idea to review your insurance regularly to make sure you have the right type of cover—and enough of it.

You probably don’t think about your insurance regularly, but there are certain times when you should consider updating your policies to make sure they still reflect your lifestyle and insurance needs.

When and why you should review your insurance

Insurance works best when you have the right level of protection for your situation and as your life changes, so might your insurance needs. You should consider reviewing your cover whenever your situation changes, like:

taking on a mortgage to buy a property

having children

getting married

upsizing or downsizing your home

getting a pay rise or take a pay cut

starting a business

experiencing a change in your health or lifestyle

paying off your mortgage

stopping supporting financially dependent children

joining a new super fund that may provide automatic insurance cover

retiring.

These milestones mark important times to review your insurance, including the amount of cover you have and whether your beneficiaries (those who will receive your insurance in the event of your death) are up to date.

How to review your insurance

Insurance is flexible and can be changed to align to your needs. Below is a step-by-step guide to reviewing what you have.

Step 1: Read your insurance contract

Refer to your product disclosure statement (PDS) and read it to fully understand what you’re covered for (death, disability or injury for instance) and compare this against what you’d ideally like to be covered for.

Step 2: Check the insurance policy expiry date

Check if your insurance policy has an expiry date, and if so, make note of when it is so you’re not caught off guard. It can be a good idea to set yourself a reminder a month or two before it’s due so you can contact your insurance provider ahead of time.

Step 3: Know your beneficiaries

An insurance beneficiary is the person, or people, who will receive your insurance payout in the event of your death. It’s important to make sure your beneficiaries are up to date so your money ends up in the right hands.

Step 4: Check if you have enough insurance

To help you work out the right level of insurance cover consider the following questions.

How much money would your family have if you were to pass away or become disabled? Consider the amount of money you have in super, savings, shares and other assets, and existing insurance policies as a starting point.

How much money would your family need if you were to pass away or become disabled? Consider the size of your mortgage and any other debts you have, as well as other costs such as childcare, education and day-to-day expenses you may be covering.

The difference between these figures should provide some guidance on the amount of insurance cover you may want to have. However, you might need to compromise between what you’d like and can afford. Our AMP Insurance needs calculator can help you crunch the numbers, and you can always ask an expert for further insurance advice.

Step 5: See if you have any other insurance policies

Like many Australians, you may have insurance through super. So, it’s a good idea to check this against other policies you might have outside super.

Then compare your cover, check whether you have any insurance double ups – if you have more than one super account with the same type of insurance, you may be paying for more insurance than you need.

Something to note on your TSC insurance, you’ll most likely only be able to claim up to 75% of your pre-disability income, regardless of whether you have TSC cover within multiple super accounts.

Step 6: Compare insurance providers

If you’re not sure whether you’re getting the best deal, you might want to compare providers. Remember, there are other considerations to take into account aside from reduced premiums, such as what level of cover you get, any exclusions (like the treatment of pre-existing medical conditions) and waiting periods.

Also keep in mind if you do cancel your insurance, you might lose access to features and benefits, and you might not be able to sign back up at the same rate or with the same level of ease.

It’s also important to disclose your situation to your insurer honestly, or the policy might be invalid if you do need to make a claim.

Step 7: Reduce or manage your insurance premiums

If affordability is a major concern, speak to your super provider or insurer depending on what type of insurance you hold, to find out how you can manage your premiums without losing your policy. You might be able to:

reduce the amount you’re insured for

change how often you make a payment (If you don’t hold insurance inside super)

adjust your waiting and benefit periods.

Changing your insurance policy can be complicated, so we are here to help,If you would like to review your cover, call us on (03) 9851 0300.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-09-28 16:00:092020-09-30 05:28:54Is your insurance cover going up?

With interest rates being at record lows, you now have the best chance of making a real dent in your home loan. A small change in how you repay your home loan can make a big difference over time. By following these simple suggestions from our lending specialist Warren Richards, it is possible to reduce your debt more rapidly than ever. If you like to eliminate your debt as quickly as possible, then give Warren a call on (03) 9851 0300.

Consider paying more than the minimum

When interest rates fall it may mean it’s much easier for you to get ahead if you decide to keep paying your current repayment amount, rather than reducing to the minimum required repayment.

Take a closer look at your current home loan, and find out how well it compares

Rates and loan

features are often described on lenders websites, so this is a good place

to start researching for the right loan. Just remember that rates change

on loans and fees apply, so an interest rate is not the only measure of

good value or suitability of a home loan.

Lenders are legally

required to include a comparison rate when advertising their loan interest

rate. It is made available to help borrowers identify the true cost of a

loan and compare the costs of different loans.

Is your home loan still right for you?

Do you remember

what your life was like when you took out your home loan? Were you just

starting out buying your first home? Or maybe you had just upgraded or

even downsized. Whatever your situation, your current home loan may not

be keeping up with the way your life and circumstances have changed. There

may be features you don’t use with your current loan that you’re paying

for, or new features available that may be right for you.

Consolidating your loans

Over time, it’s easy to accumulate smaller debts here and there. They may not seem significant. But having many smaller debts could mean you’re paying a higher interest rate and multiple sets of fees. Consolidating your debts into one loan can help give you a clearer picture of what you owe and potentially save you money too. Make a list of your other loans and credit cards, their interest rates and how much they cost you. Speak to your financial adviser about consolidating your loans to potentially save you money.

A small change in how you repay your home loan can make a big difference over time. Here are some ideas to help you get started. If you think the time is right to review your current arrangements, please phone our Lending Specialist – Warren Richards, on 9851 0300”

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-09-28 16:00:022020-09-29 06:42:17Simple strategies to paying your home loan off faster