This year’s Federal Budget includes a mix of measures that impact tax, housing, investments and everyday costs. While some changes may create opportunities, others may mean it’s worth reviewing existing plans and strategies.

This overview is designed to help highlight some of the key measures that may be relevant across different stages of life. Your financial adviser can help you understand what these changes may mean for you, which measures are most relevant to your circumstances, and whether any action is worth considering.

If you are making contributions and have a retail or industry super fund, please check the fund website for cut off dates or call our office.

If you have a Self-Managed Super Fund, ensure pension payments leave the bank account by close of business on 30 June.

Action: Aim to process payments by 22 June or earlier to reduce end-of-year timing risk.

2. Review your Concessional Contributions (CC) options

The 2025–26 concessional cap is $30,000, including employer contributions, salary sacrifice and personal deductible contributions.

Action: to determine if you have any capacity, check your year-to-date total in ATO online services.

This strategy may also suit retirees or those with a large capital gains, provided they meet the contribution rules and stay within available limits, including any carried-forward concessional amounts.

3. Consider using the ‘Unused Carry Forward Concessional Contribution’ limits

If your total super balance was under $500,000 at the previous 1 July, you may be able to use unused concessional cap amounts from up to five earlier years to make extra concessional contributions.

Action: Review your unused carried-forward amounts now, especially if you still have 2020–21 amounts available before they expire after 30 June 2026.

4. Review plans for Non-Concessional Contributions (NCC) options

The 2025–26 non-concessional cap is $120,000 a year, or up to $360,000 under the bring-forward rule.

Action: consider whether contributing to the lower-balance spouse could improve tax efficiency and increase pension-phase assets.

5. Recontribution strategies

Recontribution strategies can help increase the tax-free component of super and may reduce tax on death benefits paid to non-tax dependants.

Action: Consider whether a withdrawal and recontribution before 30 June fits your cap and balance position.

6. Downsizer contributions

If you are over 55 and selling your home, you may be eligible to make a downsizer contribution of up to $300,000 per person from the sale proceeds.

Action: make the contribution within 90 days of settlement.

Used with the bring-forward non-concessional cap, this can allow a large one-year contribution, subject to eligibility and contribution limits.

7. Calculate co-contributions

If eligible, a co-contribution can be a simple way to boost your super. If your total income is equal to or less than the lower threshold and you make a non-concessional contribution of $1,000 to your super account, you will receive the maximum co-contribution of $500.

8. Examine spouse contributions and spouse contribution splitting

If your spouse’s income is below the relevant threshold, a spouse contribution may deliver a tax offset.

Action: check eligibility before contributing.

Spouse contributions can generally be used up to age 75 and count toward the receiving spouse’s non-concessional cap.

Contribution splitting may also help if one spouse has a much higher balance, if there is an age gap, or if it improves access to concessions or Age Pension outcomes.

9. Give notice of intent to claim a deduction for contributions.

If you plan to claim a tax deduction for personal concessional contributions, you must lodge a valid notice of intent to claim or vary a deduction.

Action: Submit the notice before starting a pension or taking a lump sum from the fund.

10. Review options on pension payments

Make sure the minimum pension for the year has been paid.

Age at 1 July

Standard Minimum % withdrawal

Under 65

4%

65-74

5%

75-79

6%

80-84

7%

85-89

9%

90-94

11%

95 or older

14%

Warning

Before taking any action, you should seek advice to confirm if any of the above applies to your circumstance – failure to do so may have unintended consequences.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2026-05-15 07:55:232026-05-15 07:55:27Things to consider before 30 June 2026

Tailored Lifetime Solutions has been awarded the Firm of the Year at the 2025 Count.ed Conference on Hamilton Island.

Chosen from a strong field of finalists, Tailored Lifetime Solutions was acknowledged for our professional excellence, commitment to clients and contribution to the advice community. The awards shine a spotlight on the Count network’s most outstanding firms and professionals, recognising achievement in growth, leadership, innovation and service to the financial services sector.

Andrew Kennedy, Group Executive, Wealth at Count, congratulated Tailored Lifetime Solutions on the achievement.

“These awards highlight the incredible calibre of professionals across the Count community. Tailored Lifetime Solutions has demonstrated remarkable dedication and impact, and this award is a fitting recognition of their success.”

Reflecting on the award, Tailored Lifetime Solutions said it was an honour and a Team achievement.

“At the end of the day, our main goal is to make a real difference for our clients and to help them achieve the outcomes that matter most in their lives. Having said that, it is nice to be recognise by our peers for the hard work undertaken by our Team.”

https://www.tdls.com.au/wp-content/uploads/2025/10/COUNT.ED-2025-Tribe-Dinners-0168-scaled.jpg11812560The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2025-10-02 10:59:282025-10-02 11:05:59Tailored Lifetime Solutions named Count Financial Firm of the Year

We look at how much money you might need each year and ways you can still budget for your social life.

Australian retirees generally need a certain budget each year to live a modest or comfortable lifestyle, and industry figures recently revealed the highest annual increase in those budgets since 20101.

The Association of Superannuation Funds of Australia (ASFA) put that increase, in part, down to a range of unavoidable price hikes on things such as petrol and council rates2.

If you’re in or approaching retirement, that mightn’t be welcome news, particularly if you’re prioritising bills, trying to reduce debt, helping the kids out (if you have any) and enjoying an active social life.

On the flip side, knowing how much you might need and what you may like to do could go a long way.

So, how much money do you need?

According to September 2021 ASFA figures, individuals and couples, around age 65, who are looking to retire today, would need the below annual budgets to fund certain lifestyles3.

Figures are based on the assumption people own their home outright and are relatively healthy4 .You can also see how these budgets compare to the current maximum Age Pension rates being paid by the government5.

Comfortable lifestyle

Modest lifestyle

Full Age Pension rate

Single (annual budget)

$45,238

$28,775

$25,155

Couple (annual budget)

$63,799

$41,446

$37,923

Note, a comfortable retirement lifestyle is said to enable an older, healthy retiree to be involved in a broad range of leisure and recreational activities, whereas a modest lifestyle involves just basic activities6.

How much are you likely to spend on recreation anyway?

According to figures, singles and couples around age 65, living a comfortable lifestyle in retirement, would spend about $189 and $285 of their weekly budget respectively on leisure and recreation, whereas singles and couples living a modest lifestyle would spend about $97 and $153 respectively7.

This takes into account recreational activities like8:

Movies, plays, sports and day trips

Lunches and dinners out

Club memberships

Takeaway food and alcohol

Streaming services like Netflix and Stan

Domestic vacations (and for those living comfortable lifestyles, international ones too).

What activities are on your to-do list?

Considering the above figures, it may be worth thinking about what you enjoy doing or what you’re likely to want to do more of with extra time on your hands.

The good news is, not all things will come with a price tag, so it will be possible to do a variety of things that don’t necessarily cost money.

In the meantime, here are a few simple things that you might consider to keep costs down in retirement.

Make use of your Senior’s Card for transport concessions and discounts on other goods and services

If a restaurant isn’t in your budget one week, pack a rug, basket and esky, and head out for a picnic

If you enjoy dining out, research cheaper deals on sites like Groupon and Scoopon

Have your friends over for a card night or take turns hosting simple dinner parties where people BYO

If you want to get away, look out for cheap flights or consider a road trip. There are lots in Australia

Find cheap accommodation on Airbnb, HotelsCombined, lastminute.com or consider listing your own place to earn some money while you’re away.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2022-04-12 04:12:002022-04-12 04:12:08Living costs for retirees rise at fastest pace in 10 years

A number of changes to the super system could create opportunities for Australians of all ages. Here’s a rundown of what you need to know.

Last month, the Federal Government legislated a number of proposals that it previously put forward in its May 2021 Federal Budget. The changes announced will come into effect on 1 July 2022.

Here’s a snapshot of what will change, with further details below.

More people will be eligible for contributions from their employer, under the Superannuation Guarantee (SG), as the minimum income threshold of $450 per month will be removed.

Work test requirements for those aged 67 to 75 will be softened and only apply to people who want to claim a tax deduction on voluntary super contributions they may be making.

More people will be able to make up to three years’ worth of non-concessional super contributions in the same financial year, with the cut-off age increasing from 67 to 75.

More people will be eligible to make tax-free downsizer contributions to their super from the proceeds of the sale of their home, with the eligibility age reducing from 65 to 60.

First home buyers, who meet certain criteria, will be able to withdraw an additional $20,000 in voluntary contributions from their super, to put toward a deposit on their first home.

How you could benefit from the changes

Compulsory (SG) contributions from your employer

Under the government’s Superannuation Guarantee (or SG for short), you currently need to earn at least $450 per month to be eligible for compulsory super contributions from your employer. However, from 1 July 2022 that minimum income threshold will be removed.

This means that even where an eligible employee earns less than $450 in a calendar month, there is now an obligation on the employer to make contributions. Find out more about the Super Guarantee and what you’re likely to receive if you’re eligible.

The work test

Currently, people aged 67 to 74 can only make voluntary contributions to their super if they’ve worked at least 40 hours over 30 consecutive days in the financial year, unless they meet an exemption.

From 1 July 2022, the work test will no longer apply to contributions you make under a salary sacrifice arrangement with your employer, or personal contributions that you don’t claim a tax deduction for.

Under the new rules, the work test can be met in any period in the financial year of the contribution. This is different to the current rules, where the work test must be met prior to contributing.

Non-concessional super contributions

Currently, those under the age of 67 at the start of the financial year can make up to three years of non-concessional super contributions under bring-forward rules.

From 1 July 2022, the cut-off age will increase to 75.

The bring-forward rules allow you to make up to three years of non-concessional contributions in a single year if you’re eligible. This means you could put in up to three times the annual cap of $110,000, meaning you could top up your super by $330,000 within the same financial year.

How much you can make as a non-concessional contribution will depend on your total super balance as at 30 June of the previous financial year. Find out more about bring-forward rules and how your total super balance plays a part.

Downsizer contributions

The age Australians can make tax-free contributions to their super from the proceeds of the sale of their home, which needs to be their main residence, will be reduced from 65 to 60. (Note, there is no upper age limit for downsizer contributions and no requirement to meet the work test.)

The maximum downsizer contribution amount of $300,000 per eligible person and other eligibility requirements remain unchanged.

For couples, both spouses can make the most of the downsizer contribution opportunity, which means up to $600,000 per couple can be contributed toward super. Find out more about downsizer contributions and what rules apply.

The First Home Super Save Scheme (FHSSS)

The First Home Super Saver Scheme (FHSSS) aims to provide a tax-effective way for eligible first home buyers to save for part of a deposit on a home.

Under the scheme, you can withdraw voluntary contributions (plus associated earnings/less tax) from your super fund, with the current maximum withdrawal broadly $30,000 for each eligible individual.

From 1 July 2022, this withdrawal cap will increase to broadly $50,000 for each eligible individual. Find out more about the FHSSS and what eligibility criteria applies.

The value of your investment in super can go up and down, so before making extra contributions, make sure you understand, and are comfortable with, any potential risks.

The government sets general rules around when you can access your super, which typically won’t be until you reach your preservation age (which will be between 55 and 60, depending on when you were born) and meet a condition of release, such as retirement.

Where to find help

Depending on what you want to do, you may want to speak with your adviser for more information.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2022-04-12 04:11:372022-04-12 04:11:45Super changes that could affect you from 1 July 2022

Senior economist Diana Mousina answers our questions on potential interest rate changes and what it could mean for Aussie households.

Why have interest rates been so low for so long?

The main reason interest rates have been kept so low is the Reserve Bank of Australia undershooting on its inflation target of 2-3%. We haven’t seen underlying or core inflation within that band sustainably since before 2014.

As well as inflation, a few other factors have kept growth in Australia below trend over the past decade—even before the pandemic.

Mining investment peaked back in 2012 and then after that there was a period of weaker GDP growth. Wages growth has been pretty low as well at about 2% annually when normally it should be closer to 3%.

And there’s also been spare capacity in the labour market with the unemployment rate, while not super high, probably more elevated than the RBA would like.

All these factors have kept downward pressure on rates, in line with the general experience across developed countries.

Do you think interest rates will increase in 2022?

AMP’s view is that interest rates will increase in 2022 for the first time in over 10 years. At the moment we think the first hike will probably be in August and another one in September, and by the end of the year the RBA cash rate will be up to 0.5% from 0.1%.

An earlier rate hike is possible and the earliest it could probably happen is around June. May is complicated by the upcoming federal election as the RBA usually tries to steer clear of any perception it’s influencing political outcomes. So they’ll probably try to wait until the election’s out of the way and also see what’s in the Federal Budget, although this could be a little redundant if there’s a change in government, which appears to be a distinct possibility if you believe the betting odds.

It’s important to remember that even if we do get interest rate hikes this year, the cash rate will still remain pretty low. Next year we expect more rate hikes to take the cash rate to between 1.25% and 1.5% by the end of 2023.

What are the main factors the Reserve Bank will take into account when deciding whether to raise rates?

Like most central banks around the world, the main issue here is inflation, which has been running at a much higher than expected pace.

There are a few reasons for this. The pandemic is causing disruption to supply chains and that’s leading to increases in the price of transporting goods and higher commodity prices.

There’s also been a huge increase in monetary and fiscal stimulus over the past two years, boosting demand for goods and contributing to higher prices.

While the supply chain issues are probably not going to last for ever and should start to ease off by the end of this year, it looks like the price of goods has shifted on a more long-term basis (from higher demand) and services inflation will rise as spending gets back to pre-Covid levels. As a result, we think inflation will be persistently higher than it has been over the past few years.

As well as inflation, the RBA is also looking very closely at the lower unemployment rate and signs that a pickup in wages growth is likely this year.

What do changes in interest rates mean for Australian consumers and households?

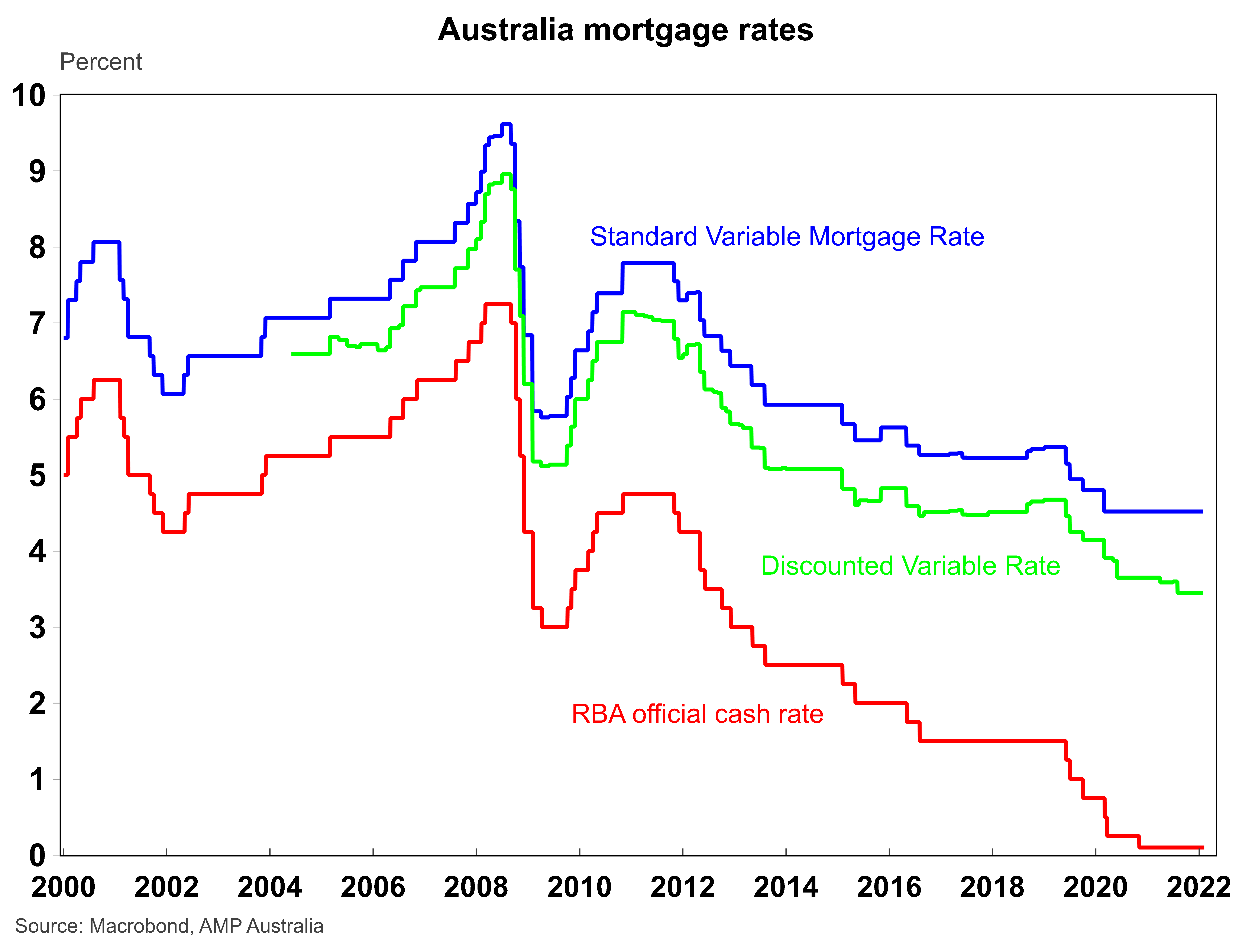

As you can see in the graph below, variable mortgage rates tend to follow the RBA cash rate so an increase in official cash rates will probably mean higher variable rates for mortgage holders.

And of course, even if you’re on a fixed interest rate for your home loan then when you roll over to a variable rate your interest rate will be higher.

So this is certainly something to take into consideration when you’re looking at your budget over the next few years.

But we think in this overall cycle any rate hike will be limited to around 200 basis points, or 2%, so we should keep it in perspective. Banks usually make sure there’s a buffer of about 2.5% when they look at serviceability of a new home loan and that’s been increased recently to 3%.

So even a 2% rate hike should be pretty sustainable for the majority of households. Naturally, like any rate increase it will probably lead to weaker home price growth and weaker consumer spending but it’s unlikely to be enough to cause a severe downturn in the Australian economy

There’s a perception Australians are too leveraged when it comes to property. Is this correct?

Pretty much so. Australia does have a very high debt to income ratio compared to other countries. Total household debt to income in Australia is 184.6% versus 101% in the United States, 175% in Canada and 124% in New Zealand, although places like Canada and New Zealand have similar housing markets in that they’ve been quite frothy over recent years, with big demand for homes and that’s increased the value of house prices there as well.

If you’re looking for positives, at least the value of the underlying assets has gone up significantly but the degree of leverage does leave households potentially exposed to higher rates.

One interesting aspect of this is that being so leveraged could act as a brake on rate hikes. It’s possible that if rates go up by 1% there’ll be a larger negative impact on the housing market and consumers than expected, so the RBA won’t be able to raise rates much further. It’s a little bit of an unknown until you get there, but at this stage we think a gradual 2% rise over the next three or four years is the most likely scenario.

What effect will any rate rise have on house prices?

It’s likely to have a negative impact but having said that, the housing market has been extremely strong during the pandemic. That’s not just because of low interest rates, it’s because of other factors increasing demand for housing—like people wanting extra room to work from home, deciding to switch to a bigger property for lifestyle factors and having spare cash they’d usually spend on travel. This has all allowed consumers to pump more money into the housing market.

Recent growth has left the housing market very exposed to rate hikes but there are already signs it’s losing a bit of steam even before any hikes.

In the first half of 2022 we expect some positive growth in house prices but over the second half of the year we expect minor falls. So for 2022 as a whole we see home prices increasing by 3% and then for 2023 we expect a fall of about 5-10%.

What does this mean for Australians paying down their mortgage?

The next few years could be a tougher time to pay your home loan off more quickly as you’ll have less ability to pay down your principal if the interest component of your loan is increasing.

How you respond really depends on your circumstances. If you know you’re going to have some spare funds or get a big windfall over the next few years, then you probably won’t want to fix 100% of your mortgage.

And what about people who are thinking of buying or selling a home?

If you need to sell your house it’s incredibly difficult to time the market—in some ways you just have to trust to luck, while doing all the usual things to make your property an attractive purchase. But in general the next few years will be a softer housing market, so if you’re thinking of selling, it might be better to do it sooner than later.

People get this idea that an interest rate hike is the end of the world. But any increases should be gradual and overall rates aren’t likely to go up by anything more than 1-2% over the next few years. And hopefully we’ll get some wages growth to offset the pain.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2022-04-12 04:11:112022-04-12 04:11:20Why Australian interest rates are likely to rise and when

Severe as they can feel, events like this aren’t permanent. Markets eventually bounce back

Super is like any type of investment, there will be times of highs and lows so it’s important to maintain a long-term perspective

By understanding your risk tolerance, you’ll be better able to make decisions about the structure of your investment portfolio in a way that aligns to you personally.

You may be concerned about the impact of Russia’s military action in Ukraine on your super.

Severe as they can feel, events like this aren’t permanent. While they can have a sharp immediate impact on investment markets, based on history, markets eventually bounce back.

If you are considering reviewing or making changes to how your super’s invested, based on these recent events, here are some things to consider.

1. Maintain a long-term perspective

Super is like any type of investment, there will be times of highs and lows. For the majority of Australians, super may be our longest-term investment given we start investing in super when we get our first job and don’t access the money until retirement.

It’s also the nature of investment markets to change rapidly, particularly shares, property or fixed income investments. The share market for example, is a public market so when the share market rises or falls, changes in share prices may impact the value of your super if it’s invested in shares.

Markets recover with time

But from what we’ve seen in the past with events that disrupt investment markets, markets do eventually recover, it just takes time.

From the 1987 Stock Market Crash to the bursting of the Tech Bubble in 2000, each trigger is different and the time it takes to recover varies too — it can take months, weeks or even years. While disruptions to markets occur fairly regularly, they are impossible to accurately predict.

So, if you do decide to make changes to your investments during falling markets—like switching to a different type of portfolio—it’s important to also consider what impact that will have on your returns when markets recover.

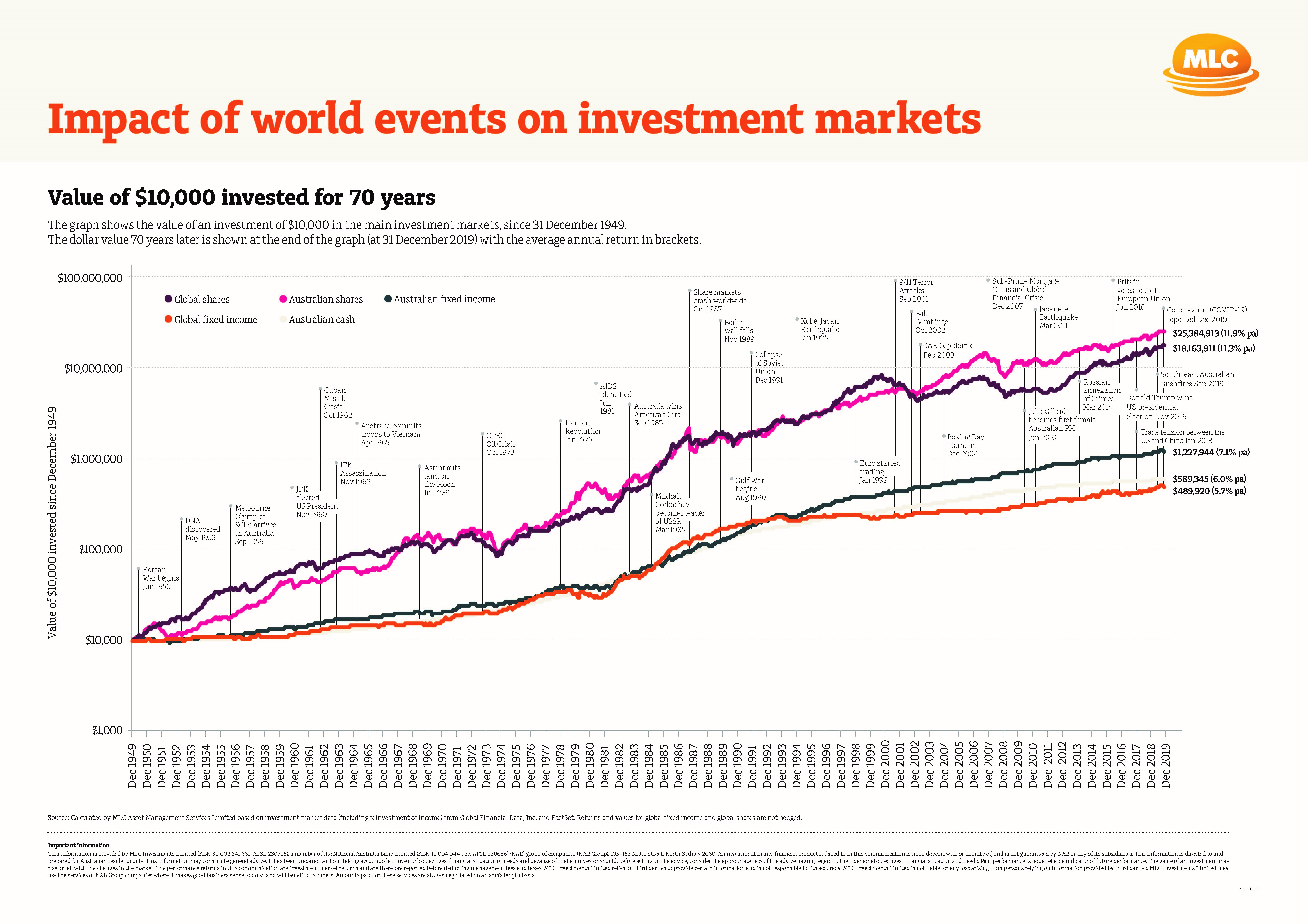

The value of $10,000 invested for 70 years

The dollar value 70 years later is shown at the end of the graph (at 31 December 2019) with the average annual return in brackets.

2. Review your investment strategy

While these events may make you want to take action, it’s important to take a moment to consider your investment strategy including why you invested that way in the first place.

Understanding the investments that make up your strategy and how they are expected to perform over long periods of time, can help you think about your strategy objectively, instead of reactively. Particularly short-term market volatility which can influence your investment decisions.

If your strategy is intended to be a long-term plan, which may be the case for those with a long way to go before they retire, making decisions based on short-term market fluctuations may greatly affect whether you achieve your long-term goals.

If you’re approaching or are in retirement, it’s still important to stay focused on your investment strategy. Carefully consider all of your options, and their impact on your retirement goals, before making any significant changes. Speaking to a financial adviser may help with this.

3. Be aware of your risk tolerance

It’s always important to consider how you feel about risk and market volatility.

By understanding your risk tolerance, you’ll be better able to make decisions about the structure of your investment portfolio in a way that aligns to you personally. Risk tolerance depends on how you feel about taking risk and your ability to do so, such as whether you are financially able to bear the risk.

Asset classes like shares and property, have higher return potential and experience greater fluctuations in value, than cash or fixed income investments. How much exposure you choose to have in each of these asset classes, may change depending on your level of comfort, especially during periods of investment market instability.

4. Consider diversification

One of the most effective ways of reducing the impacts of investment fluctuations is to diversify. Multi-asset or diversified funds invest across multiple asset classes to assist in reducing volatility.

Diversification essentially follows the concept of not putting all your eggs in one basket by spreading your money across many asset classes, countries, industries, companies, and even investment managers. When one area of your portfolio is weak and falling, another may be rising strongly. If you have money invested across many areas, changes in their values tend to balance each other out.

Diversification doesn’t mean you can avoid negative returns altogether, but it helps reduce the size and frequency of fluctuations in your portfolio. Particularly compared to if you’d only invested in shares, for instance.

5. Seek support from a professional

If you value the experience of experts in other aspects of your life, don’t discount it when it comes to managing your life savings.

A financial adviser is not just someone who helps with investments. Their job is to help you with every aspect of your financial life—savings, insurance, tax, debt—while keeping you on track to achieve your goals.

More importantly, they can answer questions like:

What age can I stop working and retire?

What strategies can I use to build my wealth?

How can I ensure my wealth is transferred to my children?

If your to-do list is endless and you never quite have time to tackle your personal finances, a financial adviser may help to set you on the right track.

Important information and disclaimer

This article has been prepared by NULIS Nominees (Australia) Limited ABN 80 008 515 633 AFSL 236465 (NULIS) as trustee of the MLC Super Fund ABN 70 732 426 024. NULIS is part of the group of companies comprising Insignia Financial Ltd ABN 49 100 103 722 and its related bodies corporate (‘Insignia Financial Group’). The information in this article is current as at March 2022 and may be subject to change. This information may constitute general advice. The information in this article is general in nature and does not take into account your personal objectives, financial situation or needs. You should consider obtaining independent advice before making any financial decisions based on this information. You should not rely on this article to determine your personal tax obligations. Please consult a registered tax agent for this purpose. Opinions constitute our judgement at the time of issue. The case study examples (if any) provided in this article have been included for illustrative purposes only and should not be relied upon for decision making. Subject to terms implied by law and which cannot be excluded, neither NULIS nor any member of the Insignia Financial Group accept responsibility for any loss or liability incurred by you in respect of any error, omission or misrepresentation in the information in this communication.

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2022-04-12 02:09:002022-04-12 04:10:54Russia and Ukraine conflict: impact on super

How’s your credit card looking after doing all the Christmas shopping? Have you made yet another New Year’s resolution to be better with your money? Whatever your situation, we could probably all do with spending a little less and saving a little more.

How to save money on bills

Avoid the lazy tax

If you’ve been with a particular provider for a while, shop around for a better deal before you continue doing business with them to avoid paying the ‘lazy tax’. It’s also worth asking your current provider what they can do to keep your business. Do some research before your policy is due to auto-renew. What you’ll get as an existing customer is unlikely to be as good a deal as what you’ll get as a new customer.

Travel insurance

With international travel off the cards, many Aussies are planning to travel at home this year. Domestic travel insurance is unlikely to cover you for COVID-19 or related travel bans. Remember the bushfires that extinguished our summer holidays last year? Well, this year, the Australian Bureau of Meteorology is predicting floods.

If you’ve paid a lot for your Aussie holiday, are hiring a rental car, or travelling with sporting equipment, you can get good value out of domestic travel insurance. But if you’ve scored a budget airfare and cheap accommodation, you might be better off claiming what you can from the airline and accommodation provider if things go awry.

Banking

Don’t pay more in fees than you have to. If you call your credit card company just before the annual fee is due and threaten to cancel the card, they may just waive it. And if you’re paying a lot of interest, switch to a low-interest credit card.

Fuel

Beat the bowser blues by doing your homework on when and where to fill up your car, and check out sites like MotorMouth which tell you which service stations currently have the lowest rates.

How to make your money go further

Special entitlements

If you’re a pensioner or hold a Health Care Card or Seniors Card, find out what benefits you can get through your local, state and federal governments or businesses. You may be able to get concessions on transport, motor vehicle registrations, rates, utilities, medications and medical supplies, animal registrations, events and movie tickets. You may also be able to have your credit card fees wiped when paying bills. Don’t hesitate to ask if any business or service offers reductions based on your having one of these cards.

Online shopping

When shopping online, especially for hotels or clothes, search around for a discount code or coupon (e.g. “hotels.com.au discount code”). New promo codes pop up all the time and there’s a bunch of websites that keep track of them. If you’re willing to sacrifice your email address, you can often get 5–10% off by signing up to a newsletter (and once that code lands in your inbox you can always smash the unsubscribe button).

https://www.tdls.com.au/wp-content/uploads/2020/12/newsletter2.jpeg16332500The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-12-23 03:31:042020-12-23 04:04:43Top money-saving tips for the new year

If cash flow is looking a tad grim this year, here are some ideas to up the presents under the tree, noting it’s the presence around it that really counts.

We don’t need to list the events of 2020 to say it’s been a big one, particularly as we approach the festive season, where many common face-to-face interactions will be limited to a phone or video call. As we grapple with a slightly different-looking Christmas, the good news is many of us will go into it with a new-found appreciation of the presence of loved ones over the presents of the material kind. In the meantime, if you’re looking for some tips around managing the costs of gift giving, here are some ways you could potentially shop a little smarter, so your money goes a little further.

Create a plan and write yourself a list While we might love the sound of ripping through wrapping paper, much of this generosity is unplanned, with nearly 75% of Aussies indicating they don’t budget for gifts, which could lead to increased pressure on household budgets well into the new year. While there’s much to be said for the spur-of-the-moment splurge, more of our generosity could be planned, with a bit of time being spent thinking about what you might buy before hitting the shops. As many events, such as Christmas, anniversaries and birthdays fall on the same day each year, it may also be somewhat easier planning for these occasions in advance.

Buy in bulk and look at cheaper alternatives Bulk buying multiple gifts that aren’t intended for a specific occasion is a growing trend, with one in three of us doing it, providing a way to save both time and money Women (31%) are more likely than men (24%) to be wise to the blessings of bulk buying, however it’s an even more popular trend among young families It also goes without saying to keep your finger on the pulse when it comes to sales. In the lead up to Christmas, there’s Click Frenzy, Black Friday, Cyber Monday, Green Monday and Free Shipping Day, not to mention Boxing Day if you happen to be seeing someone after the 25th.

Give the gift of time or skill There’s more to giving than things you can wrap – experiences matter too. Instead of another bottle of wine or a vanilla-scented candle, taking someone out for lunch, or providing a home-cooked meal, could be more up their alley. In fact, given the choice, 61% of us would opt for quality time, with only 30% preferring cash or a tangible gift. Intangible gifts are also particularly important for those aged 18 to 24, with more than half saying that an intangible gift such as time, an experience, or learning a new skill has had a more significant impact on shaping their life. On top of that, if you’re lucky enough to be going to someone else’s place this Christmas and you’ve got skills in cooking, decorating or manicuring lawns, offering these services to help with the prep work may be a highly valuable commodity for those taking on the job of hosting.

What is your Christmas shopping hack?

https://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.png00The Webmasterhttps://www.tdls.com.au/wp-content/uploads/2016/10/tls-logo-1.pngThe Webmaster2020-12-23 03:25:292020-12-23 03:25:335 ways to shop a little smarter this Christmas